1. 引言

1952年,马柯维茨首次建立了均值–方差投资组合选择模型 [1] ,使定量分析方法真正进入到了投资领域,并迅速发展起来,并取得了相当丰富的成果,朱书尚等 [2] 对现代投资组合选择的各种主要理论、模型与方法进行了系统的阐述。

马柯维茨的开创性工作对单期静态模型给出了最佳策略的显式解,但是当把此模型推广到多期情形时,由于目标函数是不可分的,无法利用动态规划方法求解,因此均值–方差多期投资组合选择问题在随后的40余年里一直没有实质性的进展。直到Li et al. (2000) [3] 提出嵌入方法,通过考虑一系列目标函数是可分的辅助问题,使得原问题得以转化,动态规划方法得以应用,才首次得到动态均值–方差组合选择问题的解析解。取得了这一突破性的进展以后,许多学者利用嵌入方法考虑了更加复杂的多期均值–方差模型。Zhu et al. (2004) [4] 考虑了带有破产限制的动态多期均值–方差组合选择模型,但由于嵌入方法需要借助一系列的辅助问题,求解过程很复杂,所以并未得到最佳目标值函数的解析表达式。郭文旌等 [5] 考虑了不确定退出时间的均值–方差问题,得到了最佳投资策略的显式表达式;Chen et al. (2011) [6] 研究了带有马氏机制转换的资产负债管理问题,也获得了最优策略;Wu et al. (2012) [7] 研究了带有马氏机制转换的非自融资情形下的均值–方差组合选择问题,利用嵌入方法得到了最优策略。刘利敏等 [8] 考虑了连续时间下的基准过程的均值–方差最优投资策略问题,得到了有效前沿。刘亚光 [9] 用中国当前金融市场股票的价格数据,对均值–方差理论进行了实证研究,得到了中国股市的有效前沿。

最近Cui et al. (2014) [10] 提出用mean-field 方法解决均值–方差组合选择问题,并且考虑了带有破产限制的多期均值–方差组合选择模型问题,该方法能够直接求解,极大地简化了求解过程,成功地获得了该问题的最佳策略以及目标值函数的显式表达式。本文受此启发,利用mean-field方法考虑有负债的多期非自融资的投资选择问题,通过扩大状态空间和策略空间,从而可以应用条件期望的平滑性质,进而利用动态规划原理得出最佳策略与有效前沿。

2. 模型的建立

假设投资者从0时刻开始进市场进行投资,计划在T时刻终止其投资管理活动。该投资者的初始财富值与初始负债分别为 与

与 ,其在t时刻的财富值与负债分别用

,其在t时刻的财富值与负债分别用 与

与 表示,其协方差设为

表示,其协方差设为 ,

, 假设投资者在n + 1种证券上进行投资,其中第0种为无风险证券,其余n种为风险证券,其在第t阶段的收益率分别为:

假设投资者在n + 1种证券上进行投资,其中第0种为无风险证券,其余n种为风险证券,其在第t阶段的收益率分别为: ,

, ,...,

,..., ,令

,令 ,假设

,假设 与

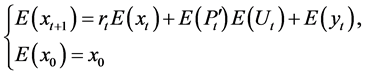

与 独立。设投资者负债的动态为 [6] :

独立。设投资者负债的动态为 [6] : ,

, ,

, 与

与 ,

, 均独立。设投资者在t时刻配置到第i个证券的资金为

均独立。设投资者在t时刻配置到第i个证券的资金为 ,令

,令 ,

, 与

与 也独立。

也独立。 为投资者的资产负债动态管理策略。以上假设均为均值–方差投资组合模型的标准假设。

为投资者的资产负债动态管理策略。以上假设均为均值–方差投资组合模型的标准假设。

本文考虑有随机现金流的情况,假设投资者在各个阶段有可能追加新的资金或抽走部分原有资金 [7] 。设其在第t阶段追加或抽走的资金用随机变量 表示,本文考虑相对简单的情形,即

表示,本文考虑相对简单的情形,即 是独立的,且

是独立的,且 与

与 ,

, 独立。进一步可以讨论不独立的情形,这将在以后的工作中进一步完善。设

独立。进一步可以讨论不独立的情形,这将在以后的工作中进一步完善。设 ,于是投资者的总盈余过程可以表示为:

,于是投资者的总盈余过程可以表示为:

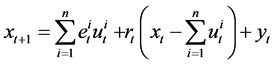

其中总财富动态为:

其中总财富动态为:

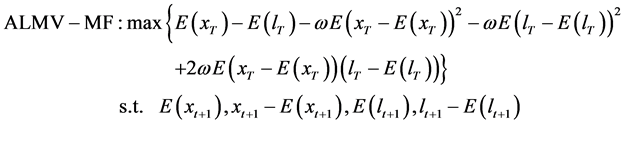

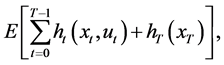

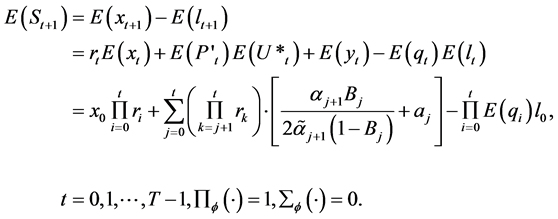

投资者将按照均值–方差准则优化总盈余资产,于是此多期均值–方差资产负债问题可以表示如下:

其中 表示总盈余资产

表示总盈余资产 的均值–方差权衡(trade-off)参数。

的均值–方差权衡(trade-off)参数。

此资产–负债管理问题的状态空间是 ,控制变量空间为

,控制变量空间为 ,目标函数是不可分的,利用mean-field方法,把状态空间扩展为

,目标函数是不可分的,利用mean-field方法,把状态空间扩展为 ,控制变量空间扩展为

,控制变量空间扩展为 ,同时把目标函数重新整理,得到:

,同时把目标函数重新整理,得到:

于是在mean-field框架下,原资产–负债管理问题可写为:

分别满足动态方程(1),(2),(3),(4),

(1) (2)

(1) (2)

(3)

(3)

(4)

(4)

3. 模型的求解

为了求解此资产–负债管理问题(ALMV-MF),需要两个引理,其证明可以参考文献 [10] 。

引理1:设 ,则下式成立:

,则下式成立:

给出引理2之前,先给出相关符号表示。设多期优化控制问题的目标函数为:

表示状态变量,

表示状态变量, 表示控制变量,

表示控制变量, 。设

。设 表示状态t时刻的信息,令

表示状态t时刻的信息,令

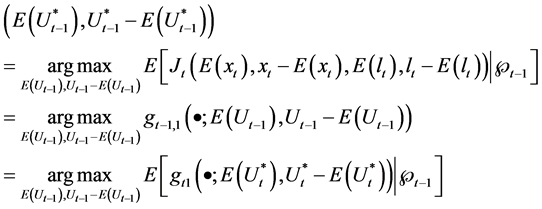

Bellman最优原理指出多期优化问题的最优策略具有如下特性 [11] :就最优策略而言,不论当前状态是由以前何种决策所造成,余下的策略对当前的状态亦必定构成最优策略,从而如果优化问题的目标函数是可分的,那么运用动态规划可将多期最优决策问题分解为一系列单期最优决策问题求解,于是t时刻的最优策略为:

(5)

(5)

而文献 [10] 则进一步利用条件期望的平滑性得到如下引理:

引理2:设多期优化控制问题中各个符号表示如上所示,

若 ,

,

其中 ,则有

,则有

(6)

(6)

注1:比较(5)、(6)两式可知:值函数 的条件期望的期望为0的部分

的条件期望的期望为0的部分 对最优策略

对最优策略 的确定没有贡献。

的确定没有贡献。

下面给出本文的主要结论。

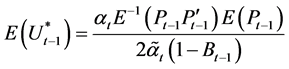

命题1:资产–负债管理问题(ALMV-MF)的最优策略为:

最佳期望盈余水平为:

其中

证明:资产–负债管理问题(ALMV-MF)的目标函数为:

,

,

故

(7)

(7)

(8)

(8)

由(5)式知:

根据Bellman最优原理,有如下递推公式:

其中 ,故

,故

其中

(9)

(9)

,考虑到“注1”,故有:

,考虑到“注1”,故有:

(10)

(10)

下面我们证明 有如下形式:

有如下形式:

(11)

(11)

(12)

(12)

当 时,即计算

时,即计算 ,为此先计算

,为此先计算 。注意(1)~(4),于是有:

。注意(1)~(4),于是有:

(13)

(13)

(14)

(14)

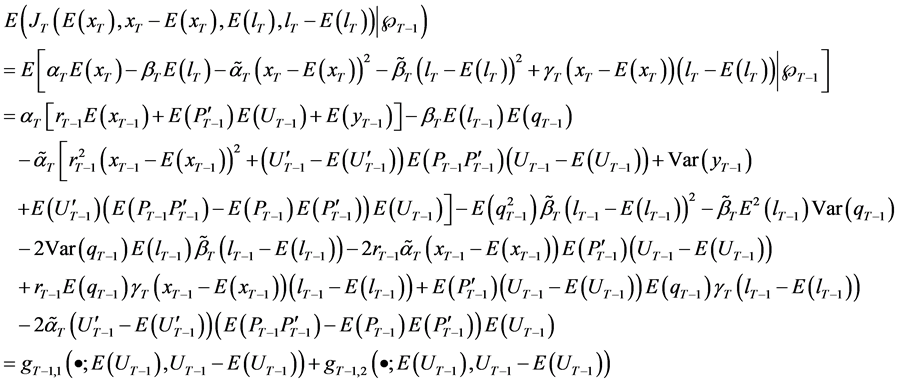

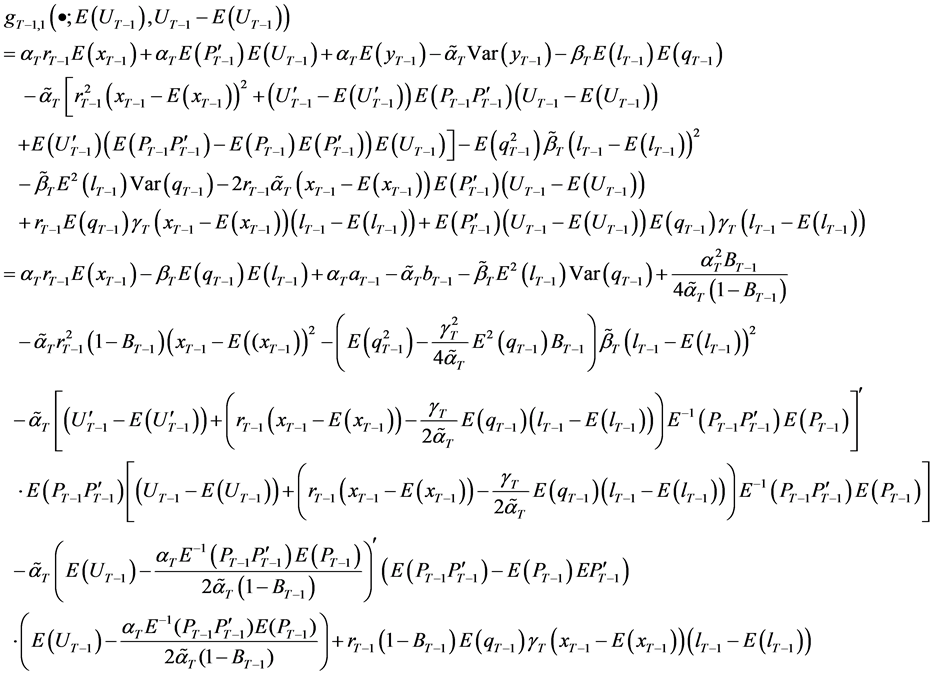

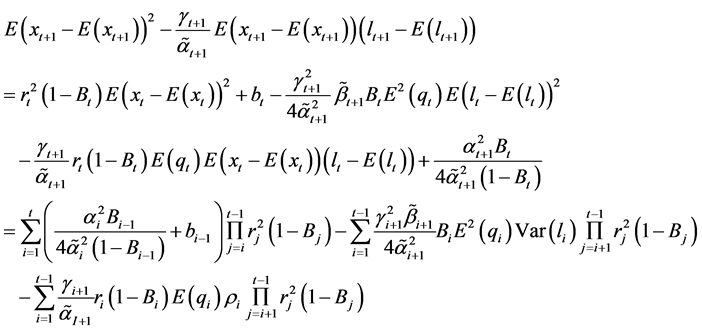

把(1)~(4)以及(13)~(14)代入(7)式并取条件期望:

(15)

(15)

其中

显然有

因为 与

与 均独立,故与

均独立,故与 也独立,取条件期望后值为0,所以上式中没有

也独立,取条件期望后值为0,所以上式中没有 的相关项,同样的原因上式中也没有

的相关项,同样的原因上式中也没有 、

、 的相关项。

的相关项。

由(15)式知:

(16)

(16)

由(10)式知:

于是由(16)式可推得知 时刻的最佳策略:

时刻的最佳策略:

,

,

,

,

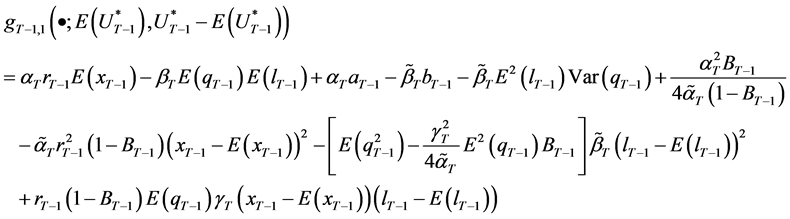

把最佳策略代回(16)式得:

结合(8)式知, 满足(11)-(12)式。

满足(11)-(12)式。

下面用数学归纳法证明(11)~(12)式对于 都成立。现在已知,当

都成立。现在已知,当 时,(11)~(12)式成立,我们假设(11)~(12)式对

时,(11)~(12)式成立,我们假设(11)~(12)式对 成立,即

成立,即 满足(11)~(12)式,证明(11)~(12)式对

满足(11)~(12)式,证明(11)~(12)式对 也成立。既然(11)~(12)式对

也成立。既然(11)~(12)式对 成立,则由(9)式可得,

成立,则由(9)式可得,

进行与(15)~(16)式类似的推导,并注意

可得:

(17)

(17)

,

,

且把最优策略 代入

代入 ,并注意(8)式,得到

,并注意(8)式,得到 也满足(11)~(12)式。

也满足(11)~(12)式。

利用(1),(3),(17)计算得到 :

:

(18)

(18)

证毕。

由命题1可得资产–负债管理问题在t时刻的最优策略为:

其中 由(12)式给定

由(12)式给定

为求有效前沿,还须计算 。

。

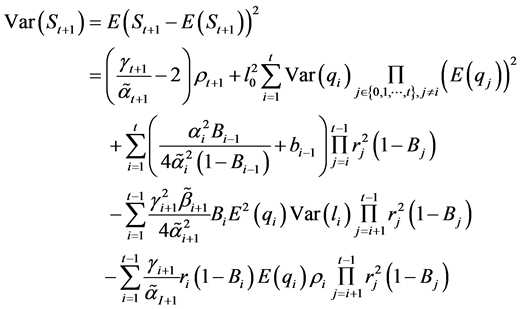

于是得到 的表达式:

的表达式:

(19)

(19)

其中 由(12)式给定,都依赖于

由(12)式给定,都依赖于 ,结合(18),(19)式消去参数

,结合(18),(19)式消去参数 即得有效前沿。

即得有效前沿。

当 时,多期资产–负债问题简化为最经典的多期均值方差问题,参数

时,多期资产–负债问题简化为最经典的多期均值方差问题,参数 均为0,其余参数简化为:

均为0,其余参数简化为:

与文献 [9] 中相应的结论一致。

4. 结论

本文考虑有现金流追加的投资选择问题,在均值–方差模型框架下,该问题的目标函数含有盈余期望的平方这一非线性项,求解存在困难。作者利用mean-field方法,扩大了状态空间和策略空间,从而可以利用动态规划原理,进而通过迭代计算求得了最佳策略和有效前沿。

基金项目

国家自然科学青年基金(11401419);江苏省自然科学青年基金(BK20140279)。