1. 引言

合格境外机构投资者(QFII)制度是指一国在货币未实现完全可自由兑换、资本项目尚未开放的情境下,限制性地引入外汇资金、放开资本市场的一项过渡性的制度。2002年12月1日,中国证监会和中国人民银行联合颁布于同年11月7日的《合格境外机构投资者境内证券投资管理暂行办法》正式生效;《办法》实施当日,上交所与深交所各自的《合格境外机构投资者境内证券交易细则》也相继出台,表示QFII制度在我国逐步步入实操阶段。随着我国资本市场开放程度的逐步提高,对QFII管制的进一步放松,QFII的额度审批和资质审批规模逐渐扩大,愈来愈多的合格境外机构投资者获得QFII的资格认定进入我国,获得认定的QFII家数从2003年二季度的3家,增加到2014年三季度的260家,审批额度也从最初的17亿美元扩大到640.14亿美元。

随着QFII获批额度的日渐扩大,QFII已是我国股票市场重要的参与者。至2006年初,QFII持有的股票市值为240多亿元,达到流通股票市值的0.49%,成为股票市场第二大投资机构。到2012年初,QFII持有股票市值为A股流通股票市值的1.09%,在众多投资机构中名列第三。QFII在2014年三季度持有股票的市值若剔除因限售股解禁的股票市值比二季度增加了7.41%,创下历史最高水平。由于我国引入的合格境外机构投资者都是享有声誉、成熟的投资者,其投资行为是否合理,在某种程度上对我国投资者起到一定的示范作用,对资本市场的稳定与经济的健康发展将产生重要影响。反之,则对资本市场产生不良的影响。

常见的投资者交易行为主要有惯性反转行为、窗饰行为、选股偏好、羊群行为等。其中,羊群行为作为一种投资行为存在于证券市场上,会使股票价格严重偏离公司价值,将降低价格发现的速度,加剧市场的不稳定性。如果QFII中存在羊群效应,则其对我国资本市场的不良影响不可忽视。

本文将分析QFII在我国资本市场上是否存在显著的羊群行为,比较在中国股市大环境下的不同研究时期QFII的羊群行为度随时间的变化趋势。考察QFII在我国股市是否坚持其价值投资理念,从而更好地认识QFII在我国资本市场所发挥的作用。

2. 文献综述

羊群行为的表面意思是动物成群结队地移动和觅食,后被在资本市场引用用来形容一种投资现象。羊群行为指在信息环境不能确定的时候,投资者不是基于自己的信息作出买或是卖的决定,而是选择跟随和模仿其余投资者的行为。

国外学术界最初围绕其境内机构投资者在证券市场上的羊群行为做了大量研究。Lakonishok,Shleifer,Vishny (1992) [1] 建立了LSV模型,并以1985~1989年间美国的769家股票基金为研究对象,并未发现这些基金有显著的羊群行为,只发现他们在小公司的股票买卖中有轻微的羊群行为。Wermers (1995) [2] 将LSV方法进一步改进,设计了一个组合变化测度PCM指标,使用1979~1995年的共同基金作为研究样本,发现对于规模较小的股票和成长性较好的股票,共同基金的羊群行为会比较明显。

QFII制度创立实施后,各国的学者也对QFII是否具有羊群行为做了研究。Hyuk,Kho,Stulz (1998) [3] 对韩国金融危机前后证券市场QFII行为进行分析,结果表明在韩国金融危机爆发前期,QFII的羊群行为较为显著,但在危机期间羊群行为却不显著,此时的QFII多持看空状态。Christie,Huang (1998) [4] 通过对外资股市稳定性影响以及证券市场信息效应的分析,发现QFII的投资行为对股票收益率和股价的波动有显著的影响。Kim,Wei (2002) [5] 则比较了韩国股市中国际离岸基金与其在岸母公司的交易行为,发现二者都存在羊群行为。Hsieh,Yang,Tai (2010) [6] 发现全国共同基金在受到严重金融危机冲击的国家表现出显著的正反馈交易和羊群行为,且在经济波动期间的羊群行为趋于一致。

我国学者对于我国证券市场上是否存在羊群行为的研究主要集中于以基金为首的境内机构投资者的羊群行为及其对资本市场波动的影响。祁斌,袁克等人(2006) [7] 采用LSV方法及Wermers的扩展方法,以我国证券市场上的证券投资基金为研究对象,对其交易行为做了实证分析,得出的结论也表现为我国证券投资基金之间存在比较显著的羊群行为;另外使用正负反馈操作策略,得出在流通盘较大与较小的股票上羊群行为特别显著的结论。李奇泽,张铁刚,丁焕强(2013) [8] 则更深入地研究了我国证券投资基金羊群行为的周期规律,结果显示开放式基金与封闭式基金存在周期性运行规律,基金羊群行为在不同市场板块间存在显著的“板块效应”。

国内对于QFII的羊群行为的研究比较少。刘成彦,胡枫,王皓(2007) [9] 以2004年1月到2006年3月间QFII的月度交易数据作为研究样本,重点研究了QFII在股改之前及股改期间在我国股票市场上的羊群行为程度。得出的结论表明QFII之间存在较为显著的羊群行为,尤其是在股权分置改革期间,它的羊群行为格外显著。许年行,于上尧,伊志宏(2013) [10] 从“羊群行为”视角考察和比较了境内机构投资者和QFII对于股票价格未来崩盘风险的影响,认为QFII的存在并未能改善机构投资者羊群行为和股价崩盘的正向关系。程天笑,刘莉亚,关益众(2014) [11] 分别在个股层面和行业层面比较QFII与境内机构投资者羊群行为的相互作用和相互影响,得出了QFII的行为强度明显低于境内机构投资者并倾向于跟随境内机构投资者的结论。汤敏,薜彤(2014) [12] 对从2004第四季度至2012年第三季度的30家QFII投资机构的持股明细数据进行了实证分析,发现QFII在中国证券市场上存在较为显著的羊群行为。

综上所述,在国内尽管有对机构投资者羊群行为的研究,主要还是集中在以基金为代表的机构投资者上。国内在QFII是否存在羊群行为的研究上的时间跨度比较短,QFII样本数量占比相对较少,不足以真实地反映实际的羊群行为。另外,以往研究得出的结论大多是集中于对羊群行为的总体水平的考察,而忽略了时间效应。

3. QFII投资羊群效应的实证分析

本文以QFII证券投资者为研究对象,通过他们的买卖信息和组合变化来分析其买卖过程中是否存在羊群行为。

3.1. 羊群行为度量指标选取

研究机构投资者是否存在羊群行为最经典的测量方法当属Lakonishok,Shleifer,Vishny (1992) [1] 建立的LSV模型,其衡量的指标主要是以交易双方交易量的不均衡来度量羊群行为的。为了能够衡量QFII的买方羊群行为度与卖方羊群行为度,本文还采用了Wermers (1995) [2] 提出的PCM模型中的测量买方羊群行为度和卖方羊群行为度的两个指标。也就是说,本文结合了LSV模型和PCM模型中的两个指标,同时通过引进时间维度,构建了一套动态的羊群行为度测量指标。LSV模型的具体计算公式如下:

(1)

(1)

这里i表示QFII投资者所买卖的股票, ;

; 表示在t时间段内关于i股票的羊群行为的测度。

表示在t时间段内关于i股票的羊群行为的测度。 表示在时间段t内买入股票i的QFII数量占所有买卖该股票的QFII的比例,公式如下:

表示在时间段t内买入股票i的QFII数量占所有买卖该股票的QFII的比例,公式如下:

(2)

(2)

表示在时间段t内买入股票i的QFII的数量;

表示在时间段t内买入股票i的QFII的数量; 表示在时间段t内卖出股票i的QFII的数量。

表示在时间段t内卖出股票i的QFII的数量。

为

为 的期望值,即在t时间段内买入股票i的QFII数量占买卖股票i的所有QFII数量的平均比例,也就是所有股票i的

的期望值,即在t时间段内买入股票i的QFII数量占买卖股票i的所有QFII数量的平均比例,也就是所有股票i的 值的平均值,公式如下:

值的平均值,公式如下:

(3)

(3)

为调整因子,其实质是为无羊群行为存在的原假设条件下

为调整因子,其实质是为无羊群行为存在的原假设条件下 的期望值,即

的期望值,即 ,公式如下:

,公式如下:

(4)

(4)

其中 表示时间段t内买卖股票i的QFII总家数。在QFII的交易不具有羊群行为的原假设条件下,并且QFII的决策都是互相独立的,那么任何QFII买入股票i的概率即

表示时间段t内买卖股票i的QFII总家数。在QFII的交易不具有羊群行为的原假设条件下,并且QFII的决策都是互相独立的,那么任何QFII买入股票i的概率即 服从参数为(

服从参数为( ,

, )二项式分布。当QFII买卖股票数量越大,即

)二项式分布。当QFII买卖股票数量越大,即 越大,

越大, 的值则越小。当

的值则越小。当 的值很大时,

的值很大时, 越接近于

越接近于 ,

, 即

即 的值接近于零。可见

的值接近于零。可见 与t时间段内进行股票交易的QFII的家数相关,而在无羊群行为的原假设下

与t时间段内进行股票交易的QFII的家数相关,而在无羊群行为的原假设下 可能并不一定为零,所以要减去调整因子

可能并不一定为零,所以要减去调整因子 。综上可知当

。综上可知当 显著不为零时,才存在羊群行为。

显著不为零时,才存在羊群行为。

通过LSV方法计算的结果虽然可以用来判断QFII是否具有羊群行为,但是并不具体判断QFII在交易方向买或卖的哪个方向上具有羊群行为。应用Wermers (1999) [2] 在LSV模型基础上提出的PCM模型中的 和

和 这两指标来表示买方的羊群行为度和卖方的羊群行为度。其判断公式如下:

这两指标来表示买方的羊群行为度和卖方的羊群行为度。其判断公式如下:

(5)

(5)

由以上公式可知, 表示股票i的买方羊群行为度,即QFII在时间段t内所有购入股票i的比例大于其期望值的股票;

表示股票i的买方羊群行为度,即QFII在时间段t内所有购入股票i的比例大于其期望值的股票; 表示股票i的卖方羊群行为度,即QFII在时间段t内所有购入股票i的比例小于其期望值的股票。为了进一步观察QFII羊群行为随时间动态变化的趋势,引进

表示股票i的卖方羊群行为度,即QFII在时间段t内所有购入股票i的比例小于其期望值的股票。为了进一步观察QFII羊群行为随时间动态变化的趋势,引进 ,

, ,

, 指标,计算t时期内QFII的羊群行为度。其计算公式如下:

指标,计算t时期内QFII的羊群行为度。其计算公式如下:

(6)

(6)

表示在时间段t内QFII参与交易的股票只数;

表示在时间段t内QFII参与交易的股票只数; 表示在时间段t内满足

表示在时间段t内满足 的股票只数;

的股票只数; 表示在时间段t内满足

表示在时间段t内满足 的股票只数。

的股票只数。

都只测量了t时间段内QFII对一支股票的羊群行为,为了研究QFII在整个股市中是否具有羊群行为,需要在上述研究基础上计算下文所涉及的各个时期内的平均。其计算公式如下:

都只测量了t时间段内QFII对一支股票的羊群行为,为了研究QFII在整个股市中是否具有羊群行为,需要在上述研究基础上计算下文所涉及的各个时期内的平均。其计算公式如下:

(7)

(7)

表示在时间段t内QFII参与交易的所有股票只数;

表示在时间段t内QFII参与交易的所有股票只数; 表示在时间段t内满足

表示在时间段t内满足 的股票只数;

的股票只数; 表示在时间段t内满足

表示在时间段t内满足 的股票只数。

的股票只数。

3.2. 样本的选取及处理

3.2.1. 样本的选取

本文选取的研究样本是A股市场上所有上市公司公布的前十大流通股东的QFII持仓数据,数据来源于Winds数据库。本文选择的研究跨度是从2004年第一季度到2014年第三季度,一共有43个季度,即43个考察期间。如果证明存在羊群效应,则进一步研究在股市暴涨暴跌时期QFII的羊群行为度是否会更加的显著。根据顾锋娟,金德环(2013) [13] ,选择的暴涨暴跌时期为从2005年至2009年的三个区间。

3.2.2. 数据的处理

上市公司的配股、送股、除权和转股等会对QFII持股数量产生影响,造成QFII实际买卖情况存在一定的偏差。为了减少误差,本文采用持仓数量变化占流通股的比例来判断买卖行为。其次对于在季度t对于股票i,如果参与交易的QFII低于3家,则做删除处理。因为如果一个季度内交易一只股票的QFII家数太少,会造成羊群行为度的失真,例如:只有1家买入时 ,明显会使结果偏大。由于2004年第一季度至2004年第三季度内参与交易的QFII家数都太少,做删除处理后剩下40个考察期。此外,本文还假定QFII在一个季度内对股票的交易行为都是一次完成的。本文判断QFII在某一时间段内对某一股票的买卖行为所用的方法是通过比较相邻两个季度该同一股票QFII的持股数量变化。具体来说,就是将每只股票的QFII每个季度的持股数量与上一季度进行对比,如果QFII本季度的持股数量大于上一季度,就视QFII是净买入,如果QFII本季度的持股数量小于上一季度,就视QFII是净卖出。如果QFII在上一季度股票公布的股东中未出现,而在本季度公布的股东中出现,就视QFII是净买入,如果QFII在上一季度股票公布的股东中未出现,而在本季度公布的股东中未出现,就视QFII是净卖出。

,明显会使结果偏大。由于2004年第一季度至2004年第三季度内参与交易的QFII家数都太少,做删除处理后剩下40个考察期。此外,本文还假定QFII在一个季度内对股票的交易行为都是一次完成的。本文判断QFII在某一时间段内对某一股票的买卖行为所用的方法是通过比较相邻两个季度该同一股票QFII的持股数量变化。具体来说,就是将每只股票的QFII每个季度的持股数量与上一季度进行对比,如果QFII本季度的持股数量大于上一季度,就视QFII是净买入,如果QFII本季度的持股数量小于上一季度,就视QFII是净卖出。如果QFII在上一季度股票公布的股东中未出现,而在本季度公布的股东中出现,就视QFII是净买入,如果QFII在上一季度股票公布的股东中未出现,而在本季度公布的股东中未出现,就视QFII是净卖出。

3.3. 实证分析

3.3.1. QFII羊群效应的存在性检验

首先按公式(1)计算得到了任意时期内QFII对任意一只股票的羊群行为度 ,接着由公式(5)计算得出任意时期内QFII对任意一只股票的买方羊群行为度

,接着由公式(5)计算得出任意时期内QFII对任意一只股票的买方羊群行为度 或卖方羊群行为度

或卖方羊群行为度 ,然后根据公式(6)得到了各个不同时期内QFII的平均羊群行为度

,然后根据公式(6)得到了各个不同时期内QFII的平均羊群行为度 以及其平均买方羊群行为度

以及其平均买方羊群行为度 和平均卖方羊群行为度

和平均卖方羊群行为度 ,最后由公式(7)计算得到各研究时期整体的QFII平均羊群行为度

,最后由公式(7)计算得到各研究时期整体的QFII平均羊群行为度 ,整体的QFII平均买方羊群行为度

,整体的QFII平均买方羊群行为度 和平均卖方羊群行为度

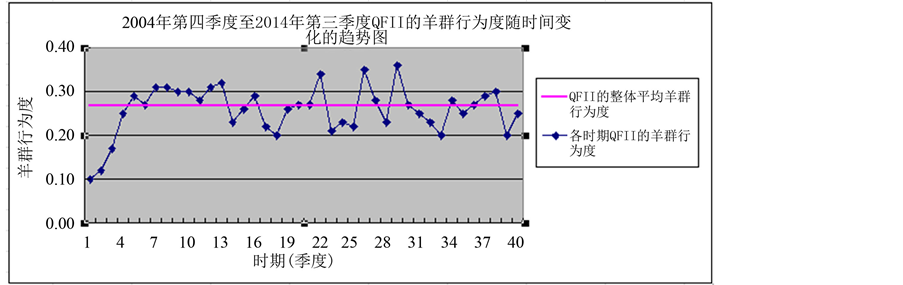

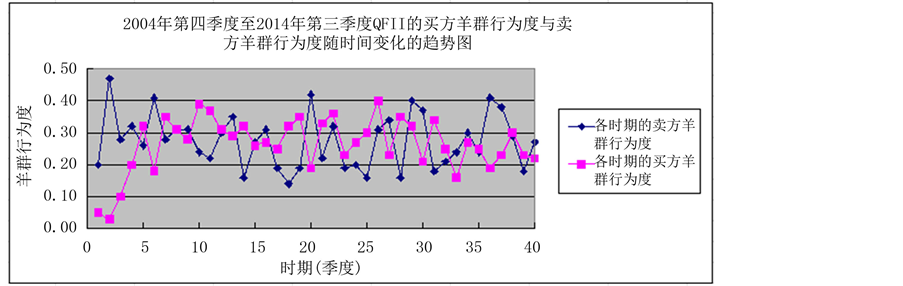

和平均卖方羊群行为度 。计算结果如将图1、图2及表1所示。

。计算结果如将图1、图2及表1所示。

从表1可知,整体考察期内QFII的平均羊群行为度 为0.2691,显著不为零,所以可以判定QFII在中国资本市场上具有显著的羊群效应。根据图1显示的趋势,前三个考察期羊群行为度明显低于平均羊群行为度,考虑是因为这三个考察期QFII制度刚实施不久,真正参与到其中的QFII投资者不是很多,所以羊群行为度会相对其他时期会比较小。其后在各个不同的考察时期内的羊群行为度的波动性比较大,但是均在平均羊群行为度上下徘徊。根据图2可知,在前四个考察季度中QFII的卖方羊群行为度远高于买方羊群行为度,随着研究时期的延长,买方羊群行为度的差距和卖方羊群行为度的差距逐渐缩小,在第四个研究时期之后,QFII的买方羊群行为度及卖方羊群行为度都出现了剧烈波动并大致上呈现的是此

为0.2691,显著不为零,所以可以判定QFII在中国资本市场上具有显著的羊群效应。根据图1显示的趋势,前三个考察期羊群行为度明显低于平均羊群行为度,考虑是因为这三个考察期QFII制度刚实施不久,真正参与到其中的QFII投资者不是很多,所以羊群行为度会相对其他时期会比较小。其后在各个不同的考察时期内的羊群行为度的波动性比较大,但是均在平均羊群行为度上下徘徊。根据图2可知,在前四个考察季度中QFII的卖方羊群行为度远高于买方羊群行为度,随着研究时期的延长,买方羊群行为度的差距和卖方羊群行为度的差距逐渐缩小,在第四个研究时期之后,QFII的买方羊群行为度及卖方羊群行为度都出现了剧烈波动并大致上呈现的是此

Figure 1. Seasonal variation of degrees of herd behavior for whole QFII

图1. QFII整体羊群行为度的季度变化

Figure 2. Seasonal variation of degrees of herd behavior for buyers and sellers of QFII

图2. QFII买方与卖方羊群行为度的季度变化

Table 1. Average degree of herd behavior for QFII during the observation period

表1. 考察期内QFII的整体平均羊群行为度

消彼长的状态,比如当QFII买方羊群行为度增加时,卖方的羊群行为度却在减少;反之则反之。另外,卖方的羊群行为度在整个时期内的平均值0.2720高于买方羊群行为度的平均值0.2660。所以从整体上来说,QFII卖方羊群行为要比买方羊群行为更加显著。

3.3.2. 比较我国股市暴涨暴跌时期QFII的羊群行为度

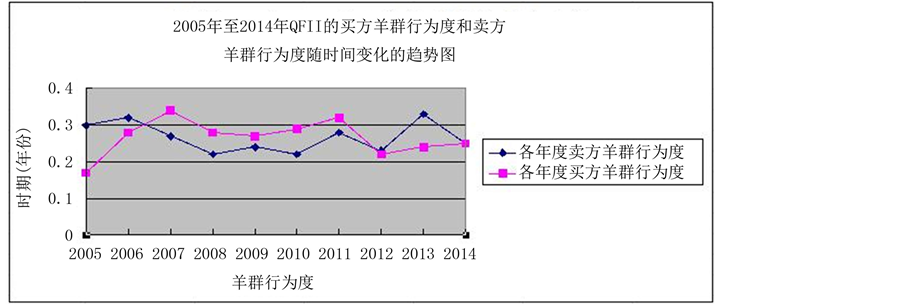

前文已经证明了QFII在中国资本市场上存在羊群行为,那么在中国股市大环境的影响下特别是在股市暴涨暴跌时期,QFII的羊群效应是否会更加显著?为此,根据计算公式(8)得出2005年至2014年每年的QFII整体平均羊群行为度,计算结果如图3和图4所示。

在我国股市历史上,大盘曾从2005年第四季度时的1087点上升至2007年第四季度的6124点,在2008年第一季度大盘从5523点下跌至2008年第四季度的1664点。根据BB牛熊市划分法发现(比如:顾锋娟,金德环(2013) [13] ),前者正好处于牛市暴涨阶段,而后者处于熊市暴跌阶段。由图3可知,从2005年到2007年QFII的羊群行为度是呈现逐渐显著的趋势。2007年股市暴涨到达高峰时,QFII羊群行为度也达到高峰。同时,图4显示的结果表明在2005年至2007年股市疯狂上涨时期,QFII买方羊群度逐渐上升,卖方羊群行为度逐渐下降,在2007年QFII买方羊群行为度达到高峰。可见QFII投资行为中

Figure 3. Degrees of herd behavior for whole QFII from 2005 to 2014

图3. 2005~2014年QFII羊群行为度变化

Figure 4. Degrees of herd behavior for buyers and sellers of QFII from 2005 to 2014

图4. 2005~2014年QFII买方和买方羊群行为度变化

存在的羊群行为会随着股市的暴涨而上升,变得更加显著。

在2008年股市暴跌时期,QFII的羊群行为度呈现下降趋势并且在2008年到达最小值。从图4的结果可知QFII买方和卖方羊群行为度在这一时期都是呈现下降的趋势,虽然买方的羊群行为度高于卖方,但是两者的差距在下降中不断缩小。可见,在我国股市暴跌时期QFII显示出投资理性且也没有对我国股市失去信心。

根据顾锋娟,金德环(2013) [13] ,股市在2008年至2009年也为牛市的大幅上涨时期。如图3显示,2008年至2009年QFII羊群行为度呈现一个小幅的上升趋势,而从图4的结果可知2008年至2009年QFII买方羊群行为是呈现下降趋势而卖方羊群行为是呈现上升趋势的,可见QFII对我国股票市场的再次上涨持有谨慎态度。

综上所述,在股市暴涨时期,QFII的买方羊群行为度上升,卖方羊群行为度下降;在股市暴跌时期,QFII的买方和卖方羊群行为度都有所下降,且两者的差距缩小;在股市暴跌后再次上涨初期,QFII的买方羊群行为呈现下降趋势,而卖方羊群行为呈现上升趋势。总之,在我国股市上QFII是有着显著的羊群效应,并且其羊群行为会受到股市涨跌大环境的影响明显。

3.4. QFII羊群效应的原因分析

根据前文对QFII羊群效应的存在性检验结果的分析,发现QFII在中国证券市场上投资的过程中确实存在羊群行为,这种行为在股市暴涨暴跌的时候表现格外显著。一直以来QFII被认为是成熟的理性的机构投资者,导致其羊群行为的原因有下面几点:

1) QFII获准额度的限制与共同的趋利性。QFII在中国证券市场上投资并非是为了造福中国,而是追求更高的利益。由于他们获准的投资额度有限,为了获取高额的回报,他们可能会选择集体有预谋的联合买入或卖出。例如在QFII的持仓数据中我们会发现,有时候会出现几家QFII会同时出现在某只流通股的前十大股东名单中,但在下一季度又集体消失的现象。尤其在股票暴涨暴跌时期,QFII可能采取抱团取暖的行为,所以羊群效应更加明显。

2) QFII共同的投资理念与高价值投资股票的有限。QFII往往具有高度一致的价值投资理念,都偏向于关注具有行业竞争优势的绩优蓝筹股和一些行业龙头股,注重安全和稳健投资。然而,我国上市公司整体水平不高,没有足够的蓝筹股和绩优股。可投资股票的有限这往往会在一定程度上造成QFII追逐相同股票的现象,从而会导致羊群行为的产生。

4. 结论与建议

研究发现,QFII在我国证券市场投资过程中具有显著的羊群效应;在股市暴涨暴跌期间,羊群效应会更加显著。在某种程度上,这反映了我国证券市场机制的不健全。为了我国证券市场的稳定发展和逐步开放,提出以下几点建议:

1) 提高对QFII的投资开放程度,拓宽其投资渠道。国内对QFII的限制比较多,QFII的投资对象仍主要是证券市场。逐渐提高期货市场及其他衍生品市场的开放程度,也会削弱QFII投资的羊群效应。

2) 培育优质股、淘汰劣质股,提高上市公司的优质度。通过扩充市场容量来提高上市公司股票质量,培育更多业绩好、管理先进、发展前景广的优质股。同时,要完善退市制度,淘汰一些业绩差、管理落后、发展前景差的劣质股。

随着QFII进入我国的数量及其在我国投资金额的持续增加,其对我国证券市场的影响力也将增大。完善我国证券市场机制,拓宽QFII的投资渠道和投资品种,可以在一定程度上制约QFII羊群行为对我国股票市场造成的负面影响,有利于我国证券市场的健康发展。